Consumers and small businesses are using credit cards more than ever before, so if you’re a business owner, one of your top priorities should be credit card fraud prevention. Hands down, one of the best ways to build your brand’s reputation, consumer trust, and ROI is by attaching a robust fraud detection system to your digital payment process.

This recommendation to invest in a fraud prevention platform is more than a sales pitch for our EVS products (though they are unparalleled in the industry). Without fraud prevention, your company is at risk of violating federal law, losing thousands or millions to illegal transactions, and ruining customer relationships and trust. Don’t gamble with the company legacy you worked so hard to build: Protect your digital transactions with fraud prevention strategies that actually work in today’s payment landscape.

Understanding The Current Payment Landscape

The modern age thrives on digital payment, but this increased reliance on online transactions leads to an increased risk of fraudulent activity. In 2022, 82% of U.S. adults owned a credit card, 50% had at least two cards in their rotation, and these cards were used to make 31% of all payments. This means that 82% of shoppers are at risk of credit card fraud, and at least 31% of your brand’s transactions could fall victim to digital crime.

Credit card debt per borrower is also at an all-time high, with consumers often maxing out cards and defaulting on balances. And consumers aren’t the only ones digging digital holes: Of the more than 33 million small businesses in the U.S., roughly 30% rely on credit card debt as a primary funding source. The bottom line?

- Credit cards aren’t going away.

- They are necessary means of payment for corporations and individuals.

- Businesses need a reliable way to help protect themselves and their consumers.

The Difficult Truth About Credit Card Fraud in 2024

Credit card fraud is on the rise – in fact, it was the most common type of identity theft last year – and cybercriminals are refining their methods of deceit with every passing year. Thanks to updated fraud prevention technology, only 10% of today’s credit card fraud comes from fraudsters stealing existing accounts.

The remaining 90% of fraudulent activity comes from new account fraud, which happens when a criminal uses your information to create a new credit card account. Increasing data breaches and synthetic account fraud are also prompting a rise in credit card fraud, causing huge losses for consumers and merchants alike.

The High Cost of Credit Card Fraud

Credit card fraud in the U.S. will lose $165.1 billion over the next 10 years, with card-not-present fraud accounting for $5.72 billion in losses. In the U.S. alone, 127 million adults have fallen victim to credit card fraud. Though card issuers typically cover over half these losses, merchants are left to bear the remaining financial burden. Plus, many small businesses who rely on credit cards for funding can also become victims of company card fraud.

In 2023, the Federal Trade Commission noted 101,427 cases of credit card fraud and 711,802 cases of credit bureau fraud – and these are just the instances that were actually reported. To break these figures down into digestible statistics, here’s what these combined 813,229 fraud cases actually mean:

- $246 million in total credit card fraud in 2023

- $34.36 billion in annual global credit and debit card fraud losses in 2022

- $305.81 billion in projected total losses due to payment card fraud from 2023 to 2030

Consumers and businesses in California, Texas, Florida, Illinois, and New York have the highest occurrences of credit card fraud, but every state across the nation is at risk. To keep your business (and your customers) protected from becoming a cybercrime statistic, you need strategic fraud prevention technology, and you need it now.

Credit Card Fraud Prevention Through Security Technologies

Criminals used to need access to a physical credit card to steal information and money, but modern payment technologies have evolved from magnetic strips to chip cards to contactless payment. While criminals have kept pace with these advancements, all is not lost. Your business can increase its digital payment security and keep its reputation, revenue, and customers safe by investing in high-quality payment verification solutions.

Today’s credit card fraud prevention platforms use machine learning to analyze a massive amount of data, polling and collecting information about user behavior, device locations, transaction details, and historical patterns to immediately identify potential fraud. Proactively incorporating fraud detection into your company’s digital payment system is the best way to enhance your digital payment security – so how can you know which payment verification solution to choose?

Is There a Robust Solution That Can Also Drive Revenue?

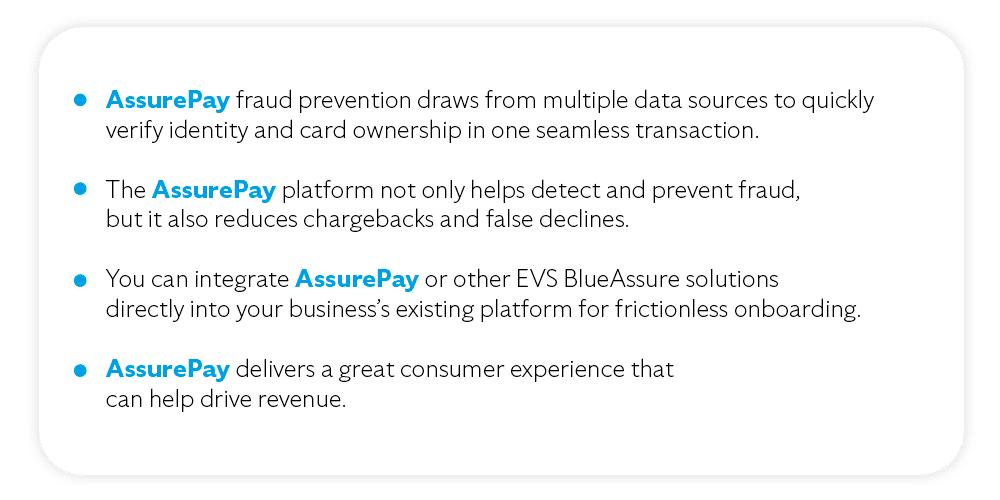

Meet AssurePay, EVS’s leading payment verification solution that keeps revenue climbing and credit card fraud at bay. AssurePay from EVS is a robust, bespoke risk mitigation strategy that delivers fast, seamless identity verification. With AssurePay in your corner, you’ll not only be able to mitigate fraud, but you’ll also increase your revenue with a seamless consumer experience and direct API integration.

Because AssurePay can be used with other products on our BlueAssure platform, your company can build a completely customized security solution. Here’s how AssurePay delivers such high-quality results:

As we noted above, AssurePay can be layered with other EVS fraud prevention products to create a bespoke security solution. Reach out to the EVS team today to explore all our BlueAssure offers, tailor a set of credit card fraud prevention strategies to your specific needs and take your business to the next level.